What is the Assquire® Grant?

The Assquire® Grant is an additional feature of Mortgage Alternative (MA) only available to first time home MA Buyers (who otherwise would or may qualify for the Queensland State Government’s First Home Owners’ Grant – and whether they apply for the State Government Grant or not).

It reduces purchase price on settlement, thereby reducing your future mortgage starting point; it is not a cash grant up front.

It is strongly argued that by providing an Assquire® grant only on extended settlement in up to ten years time, as opposed to State Government Grants on settlement in the year of contract, an Assquire® contract is better designed to assist first time buyers, WITHOUT contributing to rising house prices.

The First Home Buyer Perspective:

No one has a crystal ball on what will happen to mortgage interest rates over the next ten years, but on very reasonable projections, a special Assquire® grant + Mortgage Alternative combine to deliver a mortgage up to $20,000 to $30,000 lower in 8-10 years than if you had just met your normal mortgage repayments each month – and assuming you settle at the end of ten years with a traditional mortgage at that time.

Other Home Buyer Benefits at a Glance:

- INCREASED social benefits to getting qualifying MA FIRST home buyer applicants into their dream homes sooner

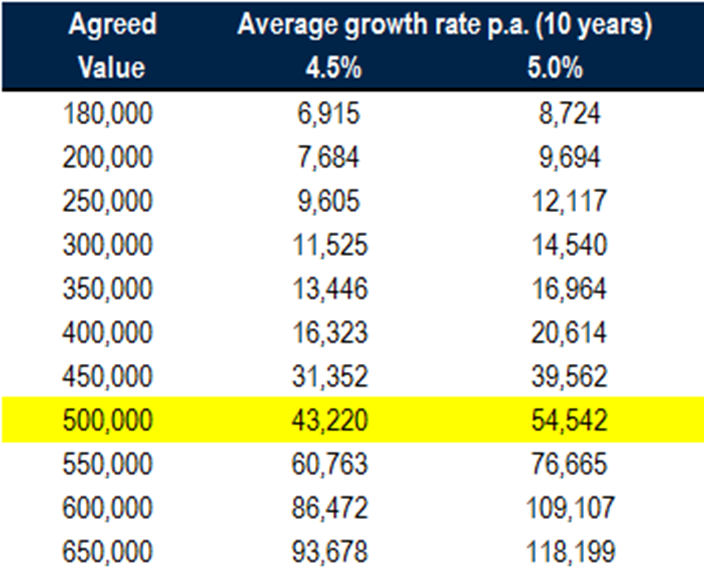

- Assquire Grant of approximately $16,000 – $54,000 for a $400,000-$500,000 home embedded into the pre-agreed contract price (compared to a non-first home buyer)

- Better designed to assist first time buyers without contributing to rising house prices

- Reduces or eliminates lenders mortgage insurance upon taking a traditional mortgage on settlement