See how Assquire benefits different types of investors

Assquire produces higher returns, faster.

The following examples give you some insight into how Assquire can benefit investors, from those working full time, to self-funded retirees.

These are simply case studies and every Assquire investment will be different, so please always seek independent professional advice before making any decisions. Incomes stated below are taxable incomes and exclude any income earned from the Assquire property in question. The investors below are non-first home buyers and have owned their investment properties for more than 12 months.

Meet Mark, 43, police officer, $80,000pa

Mark has owned a $500,000 rental property in South-East Queensland for more than 12 months. It’s geared to 70% and his bank mortgage has a variable interest rate of 5.16%.

He has used Assquire to sell and lease his property to a non-first home buyer. With property growth assumed to be an average 4.5% per annum for the duration of the Mortgage Alternative period to settlement by the buyer (at that point with a traditional mortgage), the home buyer will gain around 16-18% equity in the property. At settlement, Mark receives the proceeds and repays his own mortgage.

Our linked table provides details of Mark’s higher, faster returns by using Assquire. It shows the difference between the home buyer choosing to settle at the end of year six, and at the end of year ten. It also provides further comparisons of different taxable incomes, so that you can gain some understanding of how your own situation might relate.

Meet Fay, semi-retired, $30,000pa

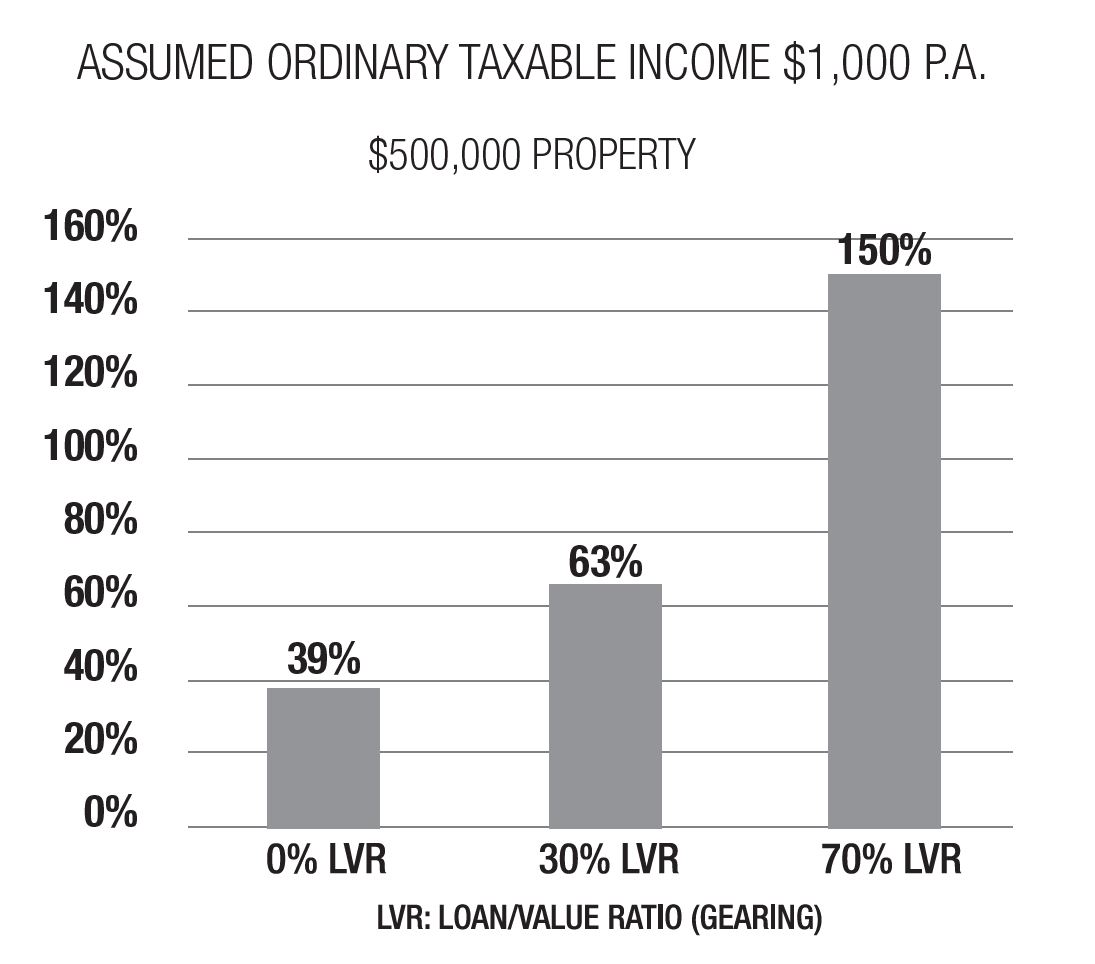

Fay is fairly new to residential property investing and bought a rental property 18 months ago to Assquire to a Mortgage Alternative buyer. Her Brisbane-based rental property was valued at $500,000. Geared to 70%, her investment return is 93% higher than what she would have achieved had she rented her property conventionally.

The table shows that had Fay geared her home to just 30%, her returns would have been 40% higher than conventional renting. So it’s certainly worth her considering (with her advisers) gearing to 70% where possible.

”Meet

The table shows that had Terry and Anne geared their home to 30%, their returns would have been 63% higher than conventional renting. So it’s certainly worth them considering (with their advisers) gearing to 70% where possible.

Meet Baz, $80,000pa

Baz is a long-term investor, earning $80,000 other taxable income. He recently borrowed 70% to purchase an investment property that is valued just under $500,000.

Baz is selling and leasing his property to first home buyers Seb and Justine who aim to settle on the property in six to ten years’ time. If they settle in ten years, Baz will enjoy 4% higher returns and will be $5,000 better off than conventional rent, at 4.5% average annual price growth. If Seb and Justine settle earlier, at six years, Baz will be $24,000 better off, with 40% higher returns than conventional rent plus average 4.5% annual capital growth. Baz loves Assquire as he reinvests his excess rental returns into his super fund semi-annually for 7% returns.

This linked table shows examples of the returns you too could achieve through Assquire, when selling and then leasing a property you have owned less than 12 months, to a first home buyer. Of course, if you can access the capital gains tax (CGT) discount for owning your investment property longer than 12 months, your returns will be even higher!

Learn how to become an Assquire investor

We’ll explain the steps involved so you are ready to go!