Financial, tax and legal advice is complex and we recommend that all Assquire investors show this answer to their adviser.

Step 1 is to apply. The first stage is free and will allow you to know whether you are likely to be accepted or not as suitable to be matched with an MA home buyer. You will need 25% equity as a minimum in your property to be conditionally suitable and you will need to furnish HRL with certain information (including statements of assets and liabilities) as part of your application.

For determining the investor’s equity, use current independent market value as a guide but the eligibility is actually based on the Agreed Value you negotiate with a future MA buyer. The 25% equity alters to 20% for Assquire Family and to 45% for self-managed superannuation funds (SMSF’s). Assquire does allow the maximum permitted security to be increased by up to a further 5% to fund part or all of any capital gains tax payable by the Assquire investor, as discussed below.

Step 2 is to confirm with your mortgage broker that you have the best rates and terms on any finance you have as an investor, and that your loans either comply with Assquire criteria, or that your affairs can (with the help of your financial adviser or accountant or both) be brought within the Assquire acceptance criteria.

Step 3 is to confirm your tax advice, as Assquire produces higher yields and may affect your lending and tax strategies. We want you to get the best possible after tax returns from your investment, and be aware of the capital gains tax consequences (see below) so that you choose the best property to Assquire, but we cannot provide you with that advice ourselves.

In preparing for step 3, you can provide your tax accountant or tax lawyer with a copy of the below example Capital Gains Tax calculation for a $500,000 sample Agreed Value home.

ASSQUIRE INVESTING

EXAMPLE SUMMARY OF CALCULATIONS PROPOSED FOR CAPITAL GAINS TAX

Please note: This example is for a landlord with a current rental property that they have owned for at least 12 months who wants to see an example of SWITCHING their current rental property after 12 months of ownership to the Assquire system, by now re-selling and leasing it to a Mortgage Alternative home buyer.

If you are an investor looking to ASSQUIRE INVEST – i.e. purchase a home conventionally today and then immediately re-sell and lease the property to a Mortgage Alternative home buyer at the earliest possible opportunity, please see the previous FAQ titled: “Do you have any example CGT calculations for new Assquire system investors purchasing a property today to resell and lease to an MA buyer?”

This is an example only current as at 20 February 2019 and should be used as a guide only.

ASSQUIRE SWITCHING BY A CURRENT LANDLORD AFTER 12 MONTHS OF OWNERSHIP & CONVENTIONAL RENTING – RESALE AND LEASE TO AN MA BUYER AT THE EARLIEST OPPORTUNITY:

Assumes a $500,000 Queensland property (and purchase by individual on $100,000 pa other taxable income) held for more than12 months and now to be resold and leased to an MA buyer

This example assumes zero change in market value up or down since the investor’s original purchase date.

- TAX RETURN – YEAR ONE SALE OF PROPERTY

|

|

|

Note |

| Sale of Assquired property proceeds |

|

580,270 |

a) |

| HRL commission ex initial deposit |

|

(13,038) |

b) |

| HRL commission ex agent’s trust account |

|

(4,515) |

c) |

| HRL settlement commission |

|

(28,723) |

d) |

| Less Cost Base (incl duty & legals) |

|

(518,420) |

e) |

| Year 1 capital gain on sale of Assquired property |

|

15,574 |

f) |

| Year 1 capital loss c/f |

|

0 |

g) |

| Profit/(Loss) |

|

15,574 |

|

| CGT discount claimed |

|

(7,787) |

h) |

| Taxable capital gain (tax payable year 2) |

|

7,787 |

|

| Tax payable – 39% |

|

(3,037) |

i) |

|

|

|

|

Assumes Investor borrowing at 75% + any CGT payable in year 2 (subject to the 5% cap discussed above).

a) Sale price is Agreed Value of $500,000 indexed by 1.5%p.a. for 10 years = $580,270 (Pre-agreed contract price)

b) Deduct HRL commission at 2.75% + GST on pre-agreed minimum purchase price deducted from initial deposit paid by MA Buyer to investor ($13,038)

c) Deduct share of HRL commission paid by investor in first 24 months from Assquire rent ($4,515)

d) Deduct: HRL settlement commission of 4.5% +GST (most of which is a licence fee paid away by HRL to IP licensor) payable by the investor on sale to MA buyer, but paid by the investor only at the end of the ten years, or on Take Early or seller default ($28,723)

e) Deduct cost base: Purchase price $500,000 + legals & duty $18,420 (prior years’ building depreciation ignored for simplicity; also excludes reduction for future building depreciation deductions, which is yet to be claimed in future tax returns) $518,420

f) Example: $500,000 home = capital gain of $15,574

g) Assume no carry forward CGT losses

h) CGT general discount (50% as at 20 February 2019) applies to reduce taxable capital gain to $7,787

i) Tax at 39% income tax rate = $3,037.

Our financial model assumes investor borrows this sum, but accelerated cash flow of average $186 per week over ten years ($73 pw in year 1) would fund this within the first eighteen months, if the investor did not borrow the CGT. Seek financial and tax advice on your own particular property and financial circumstances.

EXAMPLE END CASH FLOW END OF YEAR 10:

SETTLEMENT UPLIFT – NON-FIRST HOME BUYER ONLY:

|

|

|

Note |

| Contract of sale price |

|

580,270 |

a) |

| + Uplift to non-first home buyers only |

|

43,220 |

b) |

| Final sale proceeds of Assquired property |

|

623,490 |

|

| Less: Initial & Balance Deposit increments |

|

(58,027) |

c) |

| HRL commission on sales price uplift |

|

(1,307) |

d) |

| HRL settlement commission |

|

(13,717) |

e) |

| CGT payable to ATO |

|

0 |

f) |

| Amount available to repay borrowings |

|

550,439 |

|

| Repayment of borrowing on purchase price |

|

(375,000) |

g) |

| Repayment of borrowing to pay CGT |

|

(3,037) |

h) |

| Cash Flow to Investor End Year 10 after CGT and Borrowings |

|

172,402 |

|

a) Assumes 4.5% pa annual property price growth; sale price is Agreed Value of $500,000 indexed by 1.5% pa for 10 years = $580,270 (Pre-agreed contract price).

b) Uplift in sales price only applies if the contract’s actual average compound annual growth >= 4.5% pa. In this example, the average compound growth in property price for ten years is 4.0%pa: Uplift = $43,220.

c) Received during the period until settlement. The MA buyer deposit is paid by monthly instalments until it reaches 10% of the contract price.

d) HRL commission of 2.75% +GST on uplift of $43,220 payable at settlement– not factored into original CGT calculation in year 2 ($1,307).

e) The contract provided for HRL settlement commission of 4.5% +GST to be paid by the investor only at settlement at the end of the ten years, or on Take Early ($28,723). This commission rate reduces to 2%+GST if the contract’s actual compound annual growth rate is 4% or higher over the ten years.

Accordingly, the applicable rate is 2% + GST: HRL settlement commission = ($13,717).

Note: $28,723 was claimed in year 1 CGT as the actual capital growth rate was not known at that time.

f) CGT payable to ATO on Uplift and building depreciation recapture, less additional HRL commission on uplift payment received by investor from MA buyer. Seek advice – there are limitations on amended assessment periods.

g) Deduct: Repayment of 75% borrowing on purchase price plus incidental costs of purchase (75% of $500,000 = $375,000)

h) Deduct: Repayment of borrowing to pay CGT in year 1 ($3,037)

In the application process, once you have been conditionally credit assessed, we also provide you with our Product Specification which includes all our fee disclosures regarding commission.

Note: Should the Assquire investor default on its obligations, the contracts provide for a Notified Recovery Amount to be recoverable by the MA buyer, behind any secured position of the Assquire investor’s lender.

Your financial adviser and/or lawyer will be able to see worked examples of the Notified Recovery Amounts payable by you (or your Trustee in Bankruptcy if you default) before you sign any sale and lease contracts with an MA Buyer. So this would be good to provide to your legal and/or financial adviser, along with the Product Specification which sets out what the product is and how it works, together with a summary of fees and charges.

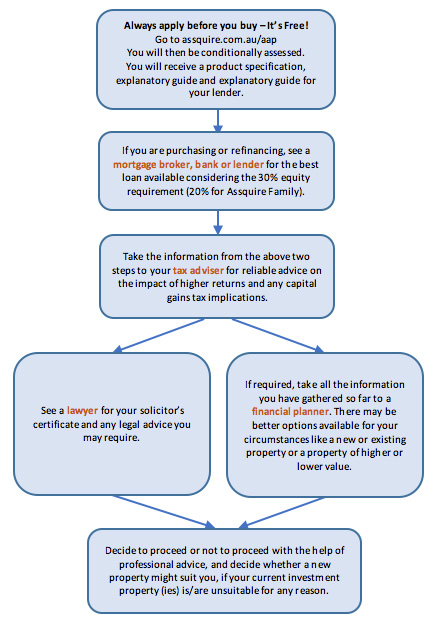

A useful chart with suggestions on how to navigate this process with the best independent advice can be found here.

DISCLAIMER:

This is an example only current as at 20 February 2019 and should be used as a guide only.

Clearly, everyone’s circumstances will be different, with different cost bases, purchase dates, and possibly Assquiring of their principal place of residence (often CGT exempt). Hence the need for independent professional tax advice.

Product pricing is subject to change without notice and may affect calculations above.

Individual investment results may vary because of interest rates, changes in taxation and other laws or regulations, whether an investor fixes their interest rates on their borrowing, whether an MA buyer settles earlier or defaults in their repayment and general economic circumstances.

Assquire investment terms may not be appropriate for an investor’s individual personal circumstances and all investors should seek independent professional legal, tax and financial advice.

Note for advisers: We have an investor comparison model – just make contact with us and we may be able to provide you with some worked examples. We will not release the financial model as we are not licensed to provide personal financial advice and it is part of our intellectual property, but we may be able to assist you as a financial adviser with certain factual information in a general (non-specific) context, to get more comfortable in providing your own independent advice to your clients on their own specific personal circumstances.

{kind=link}